What is Buy-back?

Buy-back means purchasing own shares or other specified securities by the Company from its existing shareholders or security holders.

Purpose of Buy-back

| 1. Increase in value per share |

2. Increase control of promoters

For instance;

A-Whenever a Company raises funds, it valuates the enterprise to get the value per share. When the number of shares reduces, it increases the value per share. For example: the value of enterprise is Rs. 1,00,000/– and there 1,000 share in the share capital of the Company, then value per share is Rs. 100/–. If the Company Buy-back its 200 shares then number of shares in shares capital reduced to 800 and value per share increases to Rs. 125/–.

B-The control over the company is determined by the percentage of shares held by a particular shareholder. Where non–promoter shareholders, are holding more than 50% of share capital of a Company, then promoters of the Company cannot take key decisions like appointment and removal of Directors, declaration of divided etc.

Limit of Buy-back

| Board of Directors through Board Resolution. | Upto 10% of the Paid up Equity Capital and Free Reserve. |

| Shareholders through Special Resolution. | Upto 25% of the Paid up Capital and Free Reserve. |

However, in case of Buy-back of Equity Shares, Company cannot make Buy-back exceeding 25% of Paid up Equity Capital in a financial Year.

Conditions for Buy-back

- Authorised by the Articles of Association of the Company.

- After Buy-back secured and unsecured debts of the Company cannot exceed twice of the Paid up Capital and Free Reserve. That is to say that post Buy-back Debt-Equity ratio cannot exceed 2:1.

- All the shares or other specified securities for Buy-back are fully paid-up.

- The Company cannot make Buy-back within one year from the date of completion of previous Buy-back.

- Post Buy-back the Company cannot issue same class of Shares or Securities including allotment of new Shares upto 6 months except by way of a Bonus issue or in the discharge of subsisting obligation such as conversion of warrants, Stock Option Scheme, Sweat Equity or conversion of Preference Shares or Debentures into Equity Shares.

- The Company cannot withdraw the offer once it has announced the offer to the shareholders.

- Buy-back must be completed within one year from the date of passing resolution by Board or Member, as the case may be.

- The letter of offer shall contain true, factual and material information and shall not contain any misleading information and must state that the directors of the company accept the responsibility for the information contained in such document.

- The company shall not issue any new shares including by way of bonus shares from the date of passing of special resolution authorizing the Buy-back till the date of the closure of the offer under these rules, except those arising out of any outstanding convertible instruments.

- The company shall confirm in its offer the opening of a separate bank account adequately funded for this purpose and to pay the consideration only by way of cash.

Valuation aspects

For the purpose of Buy-back the Company has to determine price of share or other specified securities, however neither Section 68 of the Act nor Rule 17 of Companies SCD Rules contains any express provisions regarding method of valuation; further the Section 247 of Act contains the general provisions in respect of valuation. The Section 147 states that where a valuation is required to be made under the Act in respect of shares, securities, property, goodwill etc. it shall be done by a registered valuer.

Nevertheless, Section 68 of the Act states that ‘NOTWITHSTANDING ANYTHING CONTAINED IN THIS ACT’ which implies that this section has an overriding effect in case of a contradiction with any other provision of Companies Act 2013.

It is to be observed that a co-joint reading of Section 68, Section 247 of the Act and Rule 17 of the Companies SCD Rules, precisely concludes that;

Valuation Report in case of Buy-back is not mandatory, however the Rule 17 of the Companies SCD Rules prescribed that the Company has to disclose the basis of Buy-back price in the explanatory statement of the General Meeting, therefore, it is advisable to get the valuation report in respect of Buy-back price from registered valuer or Chartered Accountant who has experience in valuation aspect.

Further question arises that whether a Company can make Buy-back of shares below Fair Market Value (FMV) or Book Value (for unlisted Company)?

This is a debatable question that whether a Company can Buy-back its shares below FMV or Book Value. The Companies Act, 2013 as well as Income Tax Act is salient in this matter.

Further, the ITAT Mumbai Bench in the matter of Vora Financial Services P. Ltd. [2018] 171 ITD 646 (Mum) held that buy back of shares is not covered under the ambit of section 56(2)(viia). It was observed that for the purpose of taxing Buy-back under section 56(2)(viia), shares should become “property” of recipient-company whereas in case of Buy-back, such shares are mandatorily cancelled and cannot become property of a company. Accordingly, buy back of shares should be out of the ambit of section 56(2)(viia) of the Act.

In the given case the Company had made Buy-back of shares at price below than FMV and the assessing offer of the income tax has charged income tax on such difference under Section 56(2)(viia) of the Income Tax Act.

Creation of Capital Redemption Reserve Account

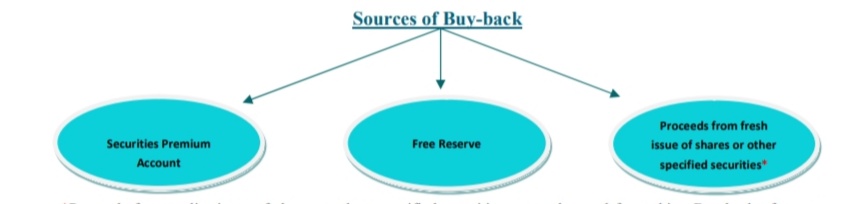

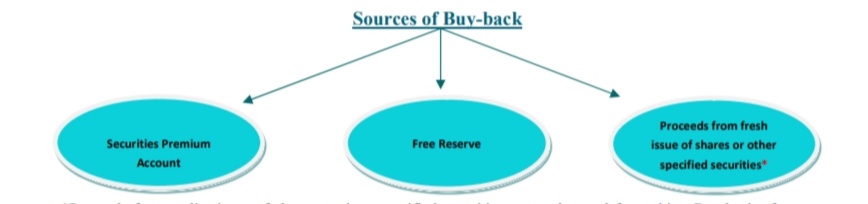

In case of Buy-back of Shares out of Free Reserve or Securities Premium Account then sum equal to nominal amount of Shares so bought back required to transfer in Capital Redemption Reserve.

Dematerialization Aspect:

Now securities of unlisted public Company are required to be kept in dematerialized form, accordingly, compliances of regulations, directions, guidelines, and circulars issued by the SEBI and Depository required to be made by the unlisted public Company. Where the unlisted public Company takes decision of Buy-back, it has to immediately inform the Depositary, Depositary Participant and Registrar & Share Transfer Agent.

Taxation Aspect

Under Section 115QA of the Income Tax Act, the Company is liable to pay tax on the amount of Buy-back of shares @20% including Surcharge and Cess (effective rate is 23.296%). Further, amount received by the shareholder in Buy-back of shares is exempted from tax under Section 10(35A) of the Income Tax Act in hands of shareholder.

©Narendra Singh, Sr. Associate, DuctusLegal ©DuctusEdge

You may download the detail article providing check list for buy buck along with procedure from the link given herein below by merely subscribing through email without any cost;

https://mehtadixit.com/wp-content/uploads/2021/01/buyback.pdf