TERM SHEET

A term sheet is the initial document i.e. signed between the investors and startup. Term sheet itself is not legally binding document but many time this document is exchanged with the confidentiality and related agreements. Although Term sheet may not be legally binding but it is like an architect plan which set forth the base for definitive agreements. Like Share Purchase agreement or Share subscription agreements. Investors project the highlights of their expectation in terms sheet and founder must critically analyse and understand the terms therein. For instance valuation, Pre or post money valuation, Anti-dilution clauses, Founders vesting and lock in, ROFR, Tag or Drag along rights etc.

TERM SHEET IN SEED AND PRE-SEED

In seed and pre-seed deals, term sheets are usually brief (often a few pages) but cover critical points that will shape the company’s ownership and control. At this stage, investments are typically minority stakes where the investor provides capital in exchange for equity (or convertible instruments) without taking full control. Key features of early-stage term sheets include the investment amount, valuation of the startup (pre-money or post-money), percentage equity to be issued, and investor rights like preferences or board representation. In contrast, later-stage VC or PE deals (e.g. a growth-stage minority VC round or a majority buyout by a PE firm) will have more elaborate term sheets. The fundamental components remain similar (investment amount, valuation, etc.), but the terms may be more investor-favorable given the larger stakes and sums involved. For instance, a majority or buyout investment term sheet might include clauses about the founder’s earn-out or retention, detailed conditions precedent, and comprehensive governance changes, since the investor plans to take control. In an early-stage context, outright buyouts are rare; most seed/VC term sheets will assume the founders continue managing the company, with the investor taking a minority stake but negotiating protective provisions for oversight. One of the most important things for founders to realize is that term sheets are usually not fully binding contracts under Indian law but they do carry certain binding commitments.

KEY TERMS UNDER TERM SHEET

A term sheet sets the tone for the detailed binding agreements to follow (such as Shareholders’ Agreements) and can heavily influence the startup’s future governance and the founders’ stake. Key features of an early stage term sheets include the investment amount, valuation of the startup (pre-money or post-money), percentage equity to be issued, and investor rights like preferences or board representation.

Indian courts generally hold that if a term sheet explicitly says it is non-binding and subject to definitive agreements, then it cannot be enforced to compel the investment or other deal actions. (For instance; OYO -ZOSTEL dispute, court refused to enforce the acquisition or award shares, noting that “enforcing a preliminary arrangement such as a term sheet particularly where key terms are yet to be agreed would undermine fundamental principles of contract law”).

What is the fundamental term in any term sheet?

Valuation and Equity stake. It determines how much of the company the founders are selling for the investment amount. Term sheets will specify either a pre-money valuation (the company’s value before the new investment) or a post-money valuation (value after including the new capital). In seed deals, pre-money is more commonly quoted. It simply means valuation of company before investment and after investment. However, it is a critical factor to consider, a misunderstanding can severely impact the percentage of stake.

A seemingly generous valuation can shrink a founder’s stake if an unaccounted ESOP pool is created post-term-sheet or if prior notes convert and dilute the equity. Founders must calculate the numbers to know what percentage founder and existing shareholders will own after the round.

ANTI DILUTION CLAUSE AND ITS CONSEQUENCES

Founders who are fortunate enough to experience their first term sheet from the investors, they must carefully make an assessment of “Anti-Dilution” clause and its long term significance on their stake as well as their venture.

So for some reason if a company is raising funds at a down round in this case under full ratchet, the earlier investor’s conversion price (for their preferred shares) is adjusted fully down to the new lower price, regardless of how many new shares are issued. This means the investor is treated as if they had invested at the new lower price all along.

Example

Investor A puts in ₹10 crore at a valuation where shares are priced at ₹100 each. They get 10 lakh preferred shares.

Later, the company faces a down-round:

New Investor B invests at ₹50 per share.

Under full ratchet:

Investor A’s earlier preferred shares are repriced at ₹50 (instead of ₹100).

So, Investor A’s shares are now treated as if they bought at the lower price, doubling their number of shares (or conversion ratio). Founder’s and employee equity gets heavily diluted, because Investor A gets more shares without putting in more money.

LIQUIDATION PREFERENCE

You are raising funds and your term sheet or SHA clause says;

“Liquidation Preference: 1x non-participating preference. A sale of all or substantially all of the Company’s assets, or a merger (collectively, a “Company Sale”), will be treated as a liquidation.”

What are the consequences?

This clause simply means your investor who has invested as CCP shares shareholder shall get a minimum amount which is equal to the amount of investment made by investor in the event of liquidation. Now don’t take it as an event which will trigger on insolvency or winding-up only and form an opinion that this clause will have almost no effect on you. No, it has. Many times investors describe the Sale or acquisition or Merger within the scope of liquidation and if your company is acquired or merged at a value less than or equal to the amount of investment in that case you will get nothing.

For example; Investor invested 15 Crore at 1X liquidation Preference and later before the conversion into equity due to multiple events resulted in acquisition of your Company in 8 crores. Now in this case founder will get Zero Money. Although the validity of this clause is subject to AOA and SHA.

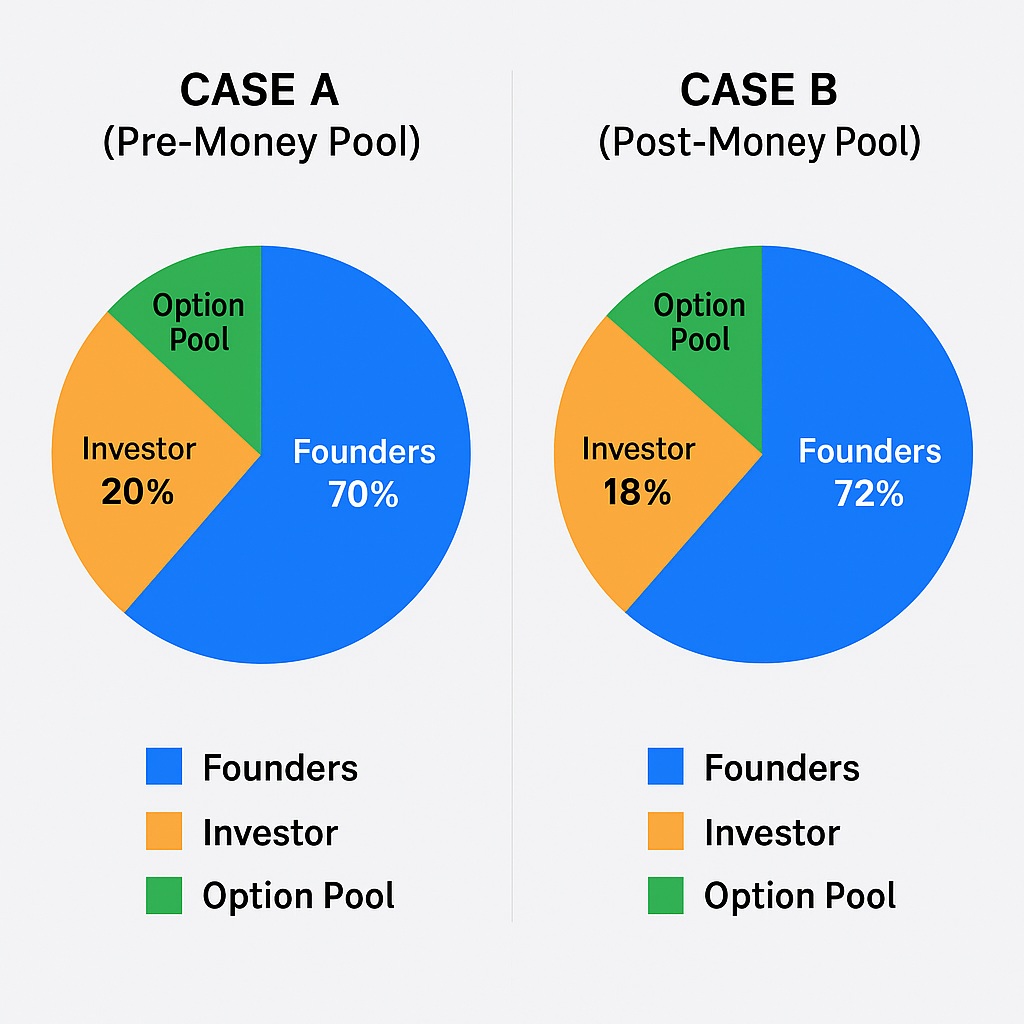

VALUATION CLAUSE UNDER TERM SHEET AND ESOP POOL

Recently, while advising a startup i realized that it is must for an angel investor or founder that they must understand the impact of option/ESOP pool in the valuation clause of your term sheet on your percentage of holding. Why?

So, in a funding term sheet “valuation clause” may say that it includes the option pool i.e. ESOP and the Post money valuation include the percentage of ESOP with an assumption that ownership is Fully diluted. (Means an assumption of ESOP that it has been fully exercised) or it may say that Option pool i.e. ESOP reserve is not included in the post money valuation and percentage of reserve shall be created thereafter.

Impact?

A. When Post Money Valuation includes the ESOP reserve in that case investor percentage is intact and founder has created a reserve out of its shareholding or out of share structure before funding. (Means ESOP Pool created before funding)

Examples: –

A. Pre-money ownership is equal to Founders 100% (₹80 Cr value) and 10% option pool is created out of founder stake. Now founder stake is 90% and Option Pool is 10%. Now Investor invests ₹20 Cr at ₹100 Cr post-money valuation and gets 20%.

B. When Post money valuation doesn’t includes ESOP reserve in that case it shall reduce the investor percentage and founder in proportion but that shall impact the investor’s interest. (Means ESOP pool created after funding)

Example: Investor puts ₹20 Cr at ₹100 Cr valuation i.e. 20% stake and now create 10% pool out of all shareholders proportionally. Now Investor share reduces from 20% → 18% and Founders reduce from 80% → 72%, wherein, Option Pool stands at 10%.

PRE-EMPTIVE RIGHTS

You invested 3 Percent in a startup as a Seed Stage investor at a valuation of 5 crores. Now Company is raising funds at a valuation of 30 Crore. How this will impact your stake?

A. In case your SHA and Term sheet had a clause for Pre-Emptive rights in that case Company has an obligation to first offer shares to you on pro-rata basis before offering to any third party.

B. Even if the clause is not available in the contract even in such instance it is a statutory obligation on the Company to first offer shares to you as specified under section 62 of the Companies act. However, AOA is the prime constitutional document which will define the scope and your right to subscribe further shares on Pro-Rata basis.

C. Intent is to give a chance to the existing shareholders to maintain their equity percentage even after fund raise.

D. In case you do not exercise the option that may result in the reduction of your equity percentage in the Company.

E. Reduction of equity percentage does not mean that you are losing as an investor. As each fund raise at a higher valuation shall result in the increase of each equity share price.

Example: You invested 3 Percent in a startup as a Seed Stage investor at a valuation of 5 crores. Now Company is raising funds at a valuation of 30 Crore. Now company will offer you shares at pro-rata basis so that you have an opportunity to maintain your equity of 3 percent.

AFFIRMATIVE VOTING RIGHTS

A very recent article in economic times says that out of the 34 startups they approached those appeared in season 4 of Shark Tank India 15 startups have not received or deliberately rejected funding due to change in circumstance or due to delay in due diligence or discrepancies found in diligence. Although Shark Tank USA itself has a funding rate of 50 percent. Among many reasons one reason which was common for few cases was “existing investors did not agree to deal terms offered on show i.e. royalty or low valuation”.

Your terms sheet and definitive agreement may have have this clause which is known as “Affirmative Voting Rights/Veto Rights. That means Company and its shareholders cannot take certain reserved decisions unless the Investor Director approves them in a Board meeting. For Instance; Amending Articles of Association (AoA) or Memorandum, Issuing new shares or changing share capital, Raising fresh debt beyond limits, Mergers, acquisitions, or asset sales.

Declaring dividends, Related party transactions, Hiring/firing key management personnel. Essentially, even if the founders have majority control at Board/Shareholder level, the investor gets a “blocking right” on certain crucial matters.

Article of Association and SHA empowers such right even for the convertible preference shares. In practice, VC/PE investors always insist on these protections to safeguard their minority position, and courts recognize them so long as they’re consistent with the Companies Act.

BOARD SEAT AND GOVERNANCE RIGHTS

The term sheet will often specify if the investor gets a Board of Directors seat or at least the right to appoint a board observer. At seed stage, some institutional investors ask for a board seat, while many angels do not. Founders should consider the implications: a board seat gives the investor direct say in company decisions. It’s common for a lead VC in Series A to get one board seat. Ensure the board structure is balanced and that you as founders keep a strong voice in governance. More critically, watch for any provisions giving investors control or veto power over decisions. Term sheets typically list “reserved matters” or protective provisions that require investor consent (even though the investor is a minority holder). Reasonable protective provisions include veto rights on issuing new shares, changing main business, incurring large debt, selling the company, etc., to protect the investor’s stake.

DRAG-ALONG AND TAG-ALONG RIGHTS

These exit-related clauses dictate what happens if some shareholders want to sell the company or their shares. Tag-along (or co-sale) usually gives minority investors the right to join a founder if the founder sells shares, ensuring the investors can tag along and sell their proportional stake on the same terms. This protects investors from being left behind, and as a founder you generally can live with tag-along as it doesn’t hurt you unless you wanted to sell your stake secretly (which you likely shouldn’t). Drag-along is more impactful: it allows majority shareholders (or a defined group, often including the investors) to force a sale of the company or force other shareholders to sell if certain conditions are met. From an investor’s view, drag-along ensures that if they find a buyer or an IPO opportunity, the founders can’t block the exit.

THINK LIKE FOUNDER- BY DUCTUS LEGAL

© DUCTUS LEGAL